Understanding Pension Tax Relief

Self-Employed in the UK

If you're self-employed, sorting a pension might not be top of your to-do list… but it really should be.

Not only are you setting yourself up for a more comfortable future, but the government actually rewards you for saving with something called tax relief.

Tax relief is the government’s way of saying “well done” for saving for retirement. When you put money into a personal pension, the government adds a bit extra based on the rate of tax you pay.

So, if you're a basic rate taxpayer and put £80 into your pension, the government adds £20 – turning it into £100 just like that

What Is Pension Tax Relief?

Pension tax relief is a benefit that reduces the amount of tax you pay when you contribute to your pension.

Essentially, the government adds money to your pension pot, boosting your savings.

For basic rate taxpayers, this means that for every £100 you contribute, the government adds an extra £25, making the total contribution £125.

How Does It Work for the Self-Employed?

As a self-employed individual, you don't have an employer to manage pension contributions, but you can still benefit from tax relief:

Basic Rate Taxpayers (20%): Your pension provider typically claims the 20% tax relief on your behalf. So, if you contribute £80, the government adds £20, totalling £100 in your pension.

Higher Rate (40%) and Additional Rate (45%) Taxpayers: You can claim additional tax relief through your Self Assessment tax return. This means you could receive an extra 20% or 25% bImageack, respectively, on top of the basic relief.

Business Contributions for Company Directors

If you operate through a limited company, your company can contribute to your pension:

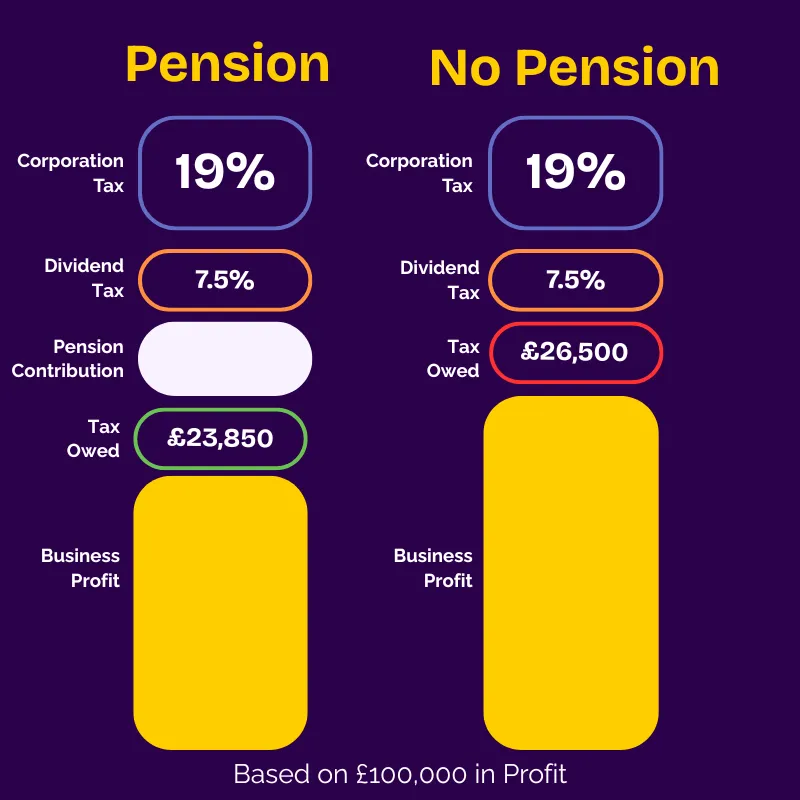

Corporation Tax Relief: Contributions made by your company are considered a business expense, reducing your corporation tax liability.

Annual Allowance: You can contribute up to £60,000 per year, or 100% of your annual earnings—whichever is lower—without incurring additional tax charges.

A £10,000 Business pension contribution means you pay £2,650 less in tax.

If you're self-employed, sorting a pension might not be top of your to-do list… but it really should be.

Not only are you setting yourself up for a more comfortable future, but the government actually rewards you for saving with something called tax relief.

Tax relief is the government’s way of saying “well done” for saving for retirement. When you put money into a personal pension, the government adds a bit extra based on the rate of tax you pay.

So, if you're a basic rate taxpayer and put £80 into your pension, the government adds £20 – turning it into £100 just like that

What Is Pension Tax Relief?

Pension tax relief is a benefit that reduces the amount of tax you pay when you contribute to your pension.

Essentially, the government adds money to your pension pot, boosting your savings.

For basic rate taxpayers, this means that for every £100 you contribute, the government adds an extra £25, making the total contribution £125.

How Does It Work for the Self-Employed?

As a self-employed individual, you don't have an employer to manage pension contributions, but you can still benefit from tax relief:

Basic Rate Taxpayers (20%): Your pension provider typically claims the 20% tax relief on your behalf. So, if you contribute £80, the government adds £20, totalling £100 in your pension.

Higher Rate (40%) and Additional Rate (45%) Taxpayers: You can claim additional tax relief through your Self Assessment tax return. This means you could receive an extra 20% or 25% back, respectively, on top of the basic relief.

Business Contributions for Company Directors

If you operate through a limited company, your company can contribute to your pension:

Corporation Tax Relief: Contributions made by your company are considered a business expense, reducing your corporation tax liability.

Annual Allowance: You can contribute up to £60,000 per year, or 100% of your annual earnings—whichever is lower—without incurring additional tax charges.

A £10,000 Business pension contribution means you pay £2,650 less in tax.

Setting Up Your Self-Employed Pension

Starting your pension plan is straightforward:

1. Choose a Pension Provider: Select a provider that suits your needs, offering flexibility and clear information on fees.

2. Determine Contribution Amounts: Decide how much you can regularly contribute, keeping in mind the tax relief benefits.

3. Set Up Contributions: Arrange for regular payments into your pension, either monthly or as lump sums.

4. Claim Additional Relief: If you're a higher or additional rate taxpayer, remember to claim your extra tax relief through your Self Assessment tax return.

Maximising Your Retirement Savings

Taking advantage of pension tax relief can significantly enhance your retirement savings.

By contributing regularly and understanding the relief available to you, you're investing in a more

secure financial future.

Setting Up Your Self-Employed Pension

Starting your pension plan is straightforward:

1. Choose a Pension Provider: Select a provider that suits your needs, offering flexibility and clear information on fees.

2. Determine Contribution Amounts: Decide how much you can regularly contribute, keeping in mind the tax relief benefits.

3. Set Up Contributions: Arrange for regular payments into your pension, either monthly or as lump sums.

4. Claim Additional Relief: If you're a higher or additional rate taxpayer, remember to claim your extra tax relief through your Self Assessment tax return.

Maximising Your Retirement Savings

Taking advantage of pension tax relief can significantly enhance your retirement savings.

By contributing regularly and understanding the relief available to you, you're investing in a more secure financial future.

Nuneaton | CV10 9JH

ICO: ZA741099

Navigate

Quick Links

Get in touch

Copyright © 2024 FleXpert Accounting | All rights reserved